Let me tell you about Gensol Engineering, a stock that’s been through a wild ride lately. As a retail investor watching this company, I’ve seen quite a drama unfold in the past few months. Once a market darling, Gensol’s stock has crashed by more than 70% in just nine months! That’s enough to make any investor break into a cold sweat.

5 Year Growth

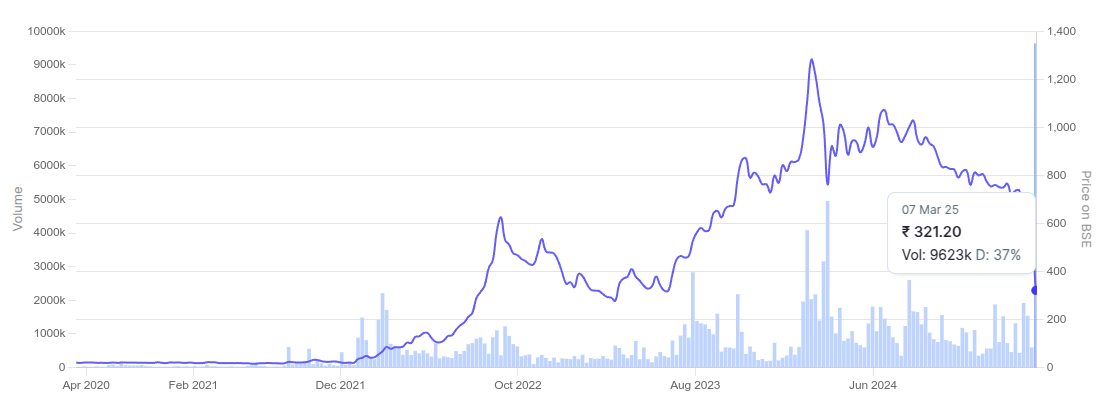

The Big Credit Rating Crash #

So what happened? In early March 2025, two credit rating agencies (CARE and ICRA) suddenly downgraded Gensol’s loans to “default” status. Basically, they said the company was having trouble paying its loans on time. Even worse, ICRA claimed Gensol had “apparently falsified” information about its debt payments. Yikes!

This news sent the stock into a nosedive, dropping 40% in just five days. The stock hit a 52-week low of ₹307.25 last Friday before slightly recovering to ₹327.

Money Problems: Too Much Debt #

The main issue here is simple - Gensol has borrowed too much money. They have debts of ₹1,146 crore but reserves of only ₹589 crore. That gives them a debt-to-equity ratio of about 1.95, which is pretty high. Every month, they need to pay about ₹20 crore just to service their debt!

What really worries me as an investor is that about 82% of the promoters’ shares are pledged as loan collateral. That’s up from 80% last September. When promoters pledge that much of their holdings, it’s usually not a good sign. And their subsidiary BluSmart Mobility isn’t doing well either - it recently defaulted on some of its own debt.

Management’s Plan to Fix Things #

To their credit, Gensol’s management hasn’t just been sitting around. They’re claiming this is just a “temporary liquidity mismatch” that’s improving as customers pay their bills. They’ve denied the “falsification” allegations and set up a committee to investigate.

They’ve also announced a plan to cut their debt by ₹665 crore by:

- Selling nearly 3,000 electric vehicles for ₹315 crore

- Selling a subsidiary company for ₹350 crore

If they pull this off, their debt-equity ratio would drop to 0.8, which would be much healthier. They say they’ve already paid off ₹230 crore of debt this year.

Shaking Things Up #

In the middle of all this, their CFO Ankit Jain resigned on March 6th, citing “personal reasons.” They quickly appointed a new CFO, Jabirmahendi Aga, who has worked with Gensol before.

The company is also taking some interesting steps to raise money:

- They’re considering a 1:10 stock split on March 13th

- They’re looking at issuing new shares and bonds

- The promoters sold 2.37% of the company (9 lakh shares) and promised to put that money back into the business

After selling those shares, the promoters still own about 60% of the company, so they definitely have skin in the game.

The Business Itself Looks Good #

Here’s what’s interesting - despite all these financial problems, Gensol’s actual business seems to be doing well! In the last quarter, their sales went up 30% to ₹345 crore, and profits increased 6% to ₹18 crore compared to the same quarter last year.

For the first nine months of the financial year, things look even better:

- Sales up 42% to ₹1,056 crore

- EBITDA (operating profit) up 89% to ₹246 crore

- Net profit up 34% to ₹67 crore

They also claim to have an order book worth ₹7,000 crore, which should mean good revenue for years to come - if they can get the money to execute these projects.

What’s Next for Gensol? #

As a retail investor watching this stock, I see several things Gensol needs to do to turn things around:

Pay their debts on time: They need to show banks and investors they can handle their loan payments consistently.

Convert orders to cash: Having a ₹7,000 crore order book sounds great, but they need money to complete these projects.

Reduce those pledged shares: The promoters need to find a way to get their shares out of hock.

Come clean about the allegations: That committee they formed needs to address the accusations about misreporting finances.

Gensol works in renewable energy and electric mobility - two sectors with massive growth potential in India. They’ve completed over 770 MW of solar projects since they started in 2012. The business model makes sense, but they’ve clearly taken on too much debt too quickly.

For me as an investor, this situation is a good reminder to look beyond just growth numbers and pay attention to things like debt levels, promoter pledging, and governance issues - especially for companies that recently moved from SME exchanges to the main market.

Will Gensol engineer a comeback? Only time will tell. But I’ll be watching their debt reduction plan closely over the next few months before making any decisions about this stock.

Disclaimer: This is not financial advice. Always do your own research before investing.